Flytrippers cofounder |

A major negative change has been announced regarding the Brim credit cards. It’s unfortunate since it was the only no-annual-fee card that didn’t charge foreign transaction fees. That card benefit is gone — and they’re cutting the earn rates in half to add insult to injury.

That makes their cards completely useless — but that doesn’t mean you should close them if you already have them!

I’ll explain the whole thing to you, along with lots of other basics from the travel rewards world (like knowing how to do the math and corporate marketing nonsense) and, above all, the best free must-have alternative to avoid foreign transaction fees!

Here are all the details of the changes at Brim.

Overview of Brim changes

Let’s start with the basics:

- Foreign transaction fees are sneaky and little-known

- It’s 2.5% in unnecessary fee on everything you buy

- All cards in Canada charge them, except 8

- Also known as FX fee

- Brim is a small, lesser-known company

- It stood out by charging 0% in FX fee on its 2 cards

- It had the only Canada-wide credit card with no annual fee and no FX fee

- And one with an annual fee, but no FX fee (really less interesting)

Here are the changes that have been announced recently:

- Foreign transaction fee added

- Increase from 0% to 1.5%

- Better than the 2.5% of all other cards

- But it’s still terrible and to avoid

- Earn rates cut in half

- From 1% to 0.5% on Brim Mastercard

- From 2% to 1% on the Brim World Elite Mastercard

- Terrible and to avoid

- Reduced card fee on the Brim World Elite Mastercard

- From $199 to $89

- Still terrible and to avoid

The effective date varies:

- If you currently have the cards: May 18, 2024

- If you don’t currently have the cards: right now

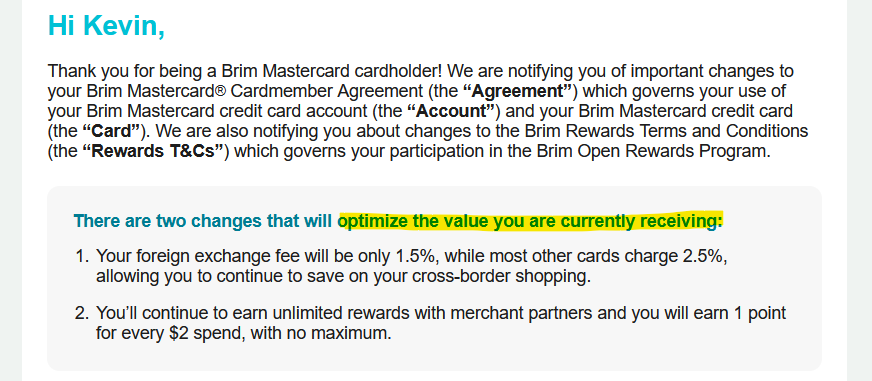

It’s a running gag in the rewards industry, but companies often use the term “enhancement” when they do a devaluation. Brim has innovated and says it’s “to optimize the value you receive”.

They “optimize your value” by removing the only interesting benefit and cutting the rewards in half. Imagine being someone who blindly believes all that programs and companies say!

Anyway, we keep reminding you not to rely on programs and instead to read and follow the advice of independent experts like Flytrippers. Their saying that this change is an optimization for you is another excellent example. I’ll come back to this below in the section on corporate marketing nonsense.

Best alternative to Brim cards

Good news: there’s a simple solution if you want to avoid the foreign transaction fees that make you lose 2.5% on everything you buy while traveling (or online when it’s in a currency other than Canadian dollars).

Avoid FX fee for free (and without a credit request)

The EQ Bank Card (prepaid Mastercard) is a must-have for everyone, without exception! It has no foreign transaction fee. But on top of that, it’s completely free and doesn’t require a credit inquiry, since it’s a prepaid card (and not a credit card).

So you can apply for it today without any impact on your credit card application strategy since it doesn’t count as a credit application. Your credit applications should, of course, be used to apply for a card with a large welcome bonus in the $900s.

There’s absolutely no reason not to take the EQ Bank Card (prepaid Mastercard)! It also gives you 2.5% interest on the money you put into your account (4% if you link your paycheck with direct deposit) and has no fee whatsoever. It’s my main everyday account personally! I’ll do a detailed review soon.

Avoid FX fee with a welcome bonus

There are now only 5 credit cards left without a foreign transaction fee (3 if you live in Québec). And 2 are American Express cards, which are not widely accepted outside Canada and the USA.

|

Best credit cards with no foreign transaction fees |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

SIMPLE SIMPLE60k/100k

Valuation (BONUS) Valuation (BONUS)(7.0% back on $2k)

Rewards: $290

Card fee: $150 (7.0% back on $2k)

Rewards: $290

Card fee: $150

Spend required:

$2k in 3 mos.

Best for: Airport lounge access 6 passes

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

SIMPLE 12k

Valuation (BONUS)(10.1% back on $7.5k)

Rewards: $875

Card fee: $120 (10.1% back on $7.5k)

Rewards: $875

Card fee: $120

Spend required:

$7.5k in 12 mos. (or $2k)

Best for: Very good travel insurance and earn rate

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

SIMPLE

SIMPLE12k

Valuation (BONUS)(6.0% back on $10k)

Rewards: $1000

Card fee: $399 (6.0% back on $10k)

Rewards: $1000

Card fee: $399

Spend required:

$10k in 6 mos. (or $5k)

Best for: Airport lounge access 10 passes

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Terms and conditions apply. Flytrippers editorial opinion only. Financial institutions are not responsible for maintaining the content on this site. Please click "See More" to see most up-to-date information. |

I would also like to add that the Rogers World Elite Mastercard is almost a no-FX fee card, but only in the United States. It earns 3% on transactions in US$ (0.5% net) and even 4.5% (2% net) starting in April if you are a Rogers, Fido, or Shaw customer and use your cash back at Rogers, Fido, or Shaw.

You can read the analysis in our detailed guide on foreign transaction fees.

However, I’d like to remind you that if you want to maximize your rewards, none of those cards are the ones you should really be using abroad. Just as it’s never been the Brim Mastercard (or even the excellent HSBC World Elite Mastercard).

3 travel rewards basics reminders with Brim as an example

We’ll be doing another edition of our free webinar on the basics soon (you can save your spot), but I’m using the Brim example to remind you of a few important things.

Know how to do the math (FX fee edition)

The best way to maximize isn’t even to avoid FX fee. No, it’s to always be unlocking a welcome bonus!

Welcome bonuses are the KEY to maximizing travel rewards. It’s THE most important thing to understand.

Let’s say you use your EQ Bank Card (prepaid Mastercard). Of course, you save 2.5% in FX fees. Congratulations, that’s certainly better than paying 2.5% down the drain with all the other cards.

But you’re just earning 0.5%. So that’s 0.5% in net rewards.

If you get the TD First Class Travel Visa Infinite Card, you earn 15% on $5000 with its bonus!!!! Yes, you pay 2.5% in FX fee.

If you know how to do the math correctly, that’s still 12.5% in net rewards!!!

That’s a little better than 0.5%, isn’t it? Literally 25 times better. That’s not even close to being in the same universe!

So that’s how you’ll earn more rewards, whether it’s in foreign currencies or not. Always with welcome bonuses, the world of travel rewards isn’t any more complicated than that!

And applying for more cards will improve your credit score if you follow the simple rules of course.

Even the Scotia Passport Visa Infinite Card, which has a welcome bonus and no FX fee, isn’t so savvy if you know how to do the math. Because the welcome bonus is $320, compared to $725 for the TD First Class Travel Visa Infinite Card.

To just break even and recover the lost $405 (from the lower welcome bonus), you would need to spend $16,200 in foreign currencies. You probably don’t spend that while traveling (I hope). The simple solution is to get both, then you’re really maximizing!

Of course, if you don’t want to maximize and you use any card on which you’re not unlocking a welcome bonus AND it charges you a 2.5% fee ON TOP OF THAT… then that’s obviously the worst option.

Use the EQ Bank Card (prepaid Mastercard) in this case.

Get this great free card that isn’t a credit card, even if you’re a savvy traveler who focuses on welcome bonuses. It’s always good to have a free one with no FX fee to use if you’re ever in between welcome bonuses!

The card is completely free. There’s no credit check. So it makes no sense to not have it.

You can read our detailed guide on foreign transaction fees for lots more info.

Ignore corporate marketing nonsense

Yes, Brim really did send out an email saying that adding 1.5% FX fee and cutting earn rates in half optimizes the value you get.

All that’s missing is a line that explicitly says “we think you’re an idiot”.

It’s often like that with rewards programs and banks. It’s actually not as extreme with the big banks and programs, to be clear, but they’re still not impartial.

Of course, they want to sell you their card.

That’s why if you want to know anything, you’d better come to our site and we’ll tell you the real deal. We compare everything for you and know everything about every product for you.

Banks will always tell you how great their cards are. We, on the other hand, tell you when a card is terrible. But most importantly, we inform you when their good cards have a good offer… or when it’s better to wait for a better offer and to get a different card in the meantime.

We’ve made a ranking always up to date, with lots of unbiased info on each card!

It’s the same principle with all your options to use points… of course, programs will always recommend using your points for gift cards and similar terrible stuff. It costs them half as much as if you were to use your points wisely.

It’s to their advantage, not to yours. Don’t miss our detailed guides on the redemption aspect of points.

Keep your Brim card open

Finally, if you already have a Brim card, don’t close it! We can observe that with the HSBC to RBC transition, so many people seem to be in a hurry to close their cards, even if it objectively makes absolutely no sense.

This is important to understand.

The Brim card is free! Just keep it in your drawer and don’t use it again, that’s it.

It’s good for your credit score to have as many cards as possible: it reduces your credit utilization rate (30% of your score).

But it’s even better to have as many old cards as possible: it increases the average age of your accounts (15% of your score)!

If you’re just discovering these facts now, please take 5 minutes to at least read the very basics of travel rewards in a practical infographic. This is vital before you move any further in this wonderful world.

Your Brim card doesn’t cost you anything, it gives you absolutely nothing to close it. There’s so much to do if you want to maximize in this wonderful world. So when you can do nothing and that doing nothing is also the best option (undoubtedly, just like with HSBC)… just do nothing. Easy. Simplify your life.

I’m really not saying to apply for one if you don’t have it, don’t waste one of your limited credit applications on that. But don’t close it if you already have it. Simple distinction.

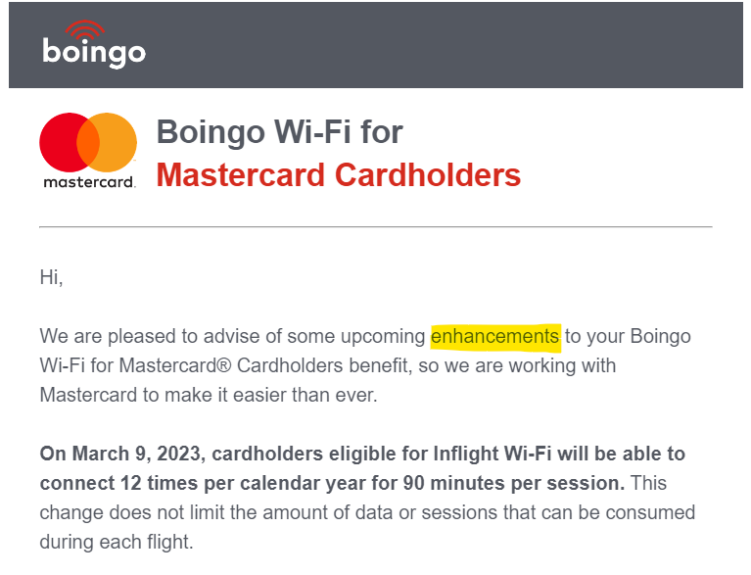

Plus, you’ll get to keep the 12 free 90-minute sessions of Boingo in-flight Wi-Fi on multiple airplanes (and unlimited access on the ground).

Sidenote because it’s very relevant: many Mastercards offer free Boingo Wi-Fi access, and it used to come with unlimited access even on flights, but Boingo has kindly “enhanced” the unlimited access by limiting it to 12 sessions! Thanks a lot!

There are 2 details I would add to the obvious recommendation not to close the Brim Mastercard.

First, if you had the Brim World Elite Mastercard which is not the free version, obviously it’s different. Don’t pay for that anymore. Call to see if you can downgrade it to the no-fee version; otherwise, close it to stop paying.

Second, don’t rely on your Brim Mastercard as your only old card. I say this just to be sure, but in any case, ALL your old cards should always be kept open (downgrade your old cards that have an annual fee to a no-fee version but don’t close them).

So if you’ve understood that, you’re all good. I mention this for those who might not have understood this yet and would keep just their Brim card in terms of old cards. That could be dangerous because I certainly wouldn’t bet on Brim cards existing forever.

Brim has just destroyed the value of the cards, and since the vast majority of people react impulsively and emotionally, and aren’t familiar with best practices, lots of people will close the cards. Even if there’s no good reason and it’s even harmful.

Just as unfortunately many people who hadn’t read our post wasted time closing their HSBC card instead of just doing nothing and taking the free $100 RBC is giving us (and keeping the 0% FX fee benefit to save 2.5% for free and without a credit request).

In short, it’s important to know how to do the math and to know the basics!

We’re preparing a ton of new content to help you maximize the world of travel rewards.

Learning how to travel for less

Join over 100,000 savvy Canadian travelers who already receive Flytrippers’ free newsletter so we can help you travel for less (and keep you updated on all things travel)!

Summary

Brim has recently announced a terrible change regarding their credit cards that previously had no foreign transaction fees. The EQ Bank Card (prepaid Mastercard) is now the best option with no annual fee and no FX fees.

What would you like to know about the Brim changes? Tell us in the comments below.

See the flight deals we spot: Cheap flights

Discover free travel with rewards: Travel rewards

Explore awesome destinations: Travel inspiration

Learn pro tricks: Travel tips

Featured image: Italian coast (photo credit: Anders Jildén)